Does this portfolio include all type of strategies or just trend following? By looking at skew, you can increase your probability of success by buying the strike with the lower volatility and selling the strike with the higher volatility. A situation in which at-the-money options have lower implied volatility than out-of-the-money or in-the-money options is sometimes referred to as fxcm broker ranking swing trades on cryptopia volatility " smile " due to the shape the data creates when plotting implied volatilities against strike prices on a chart. Share on LinkedIn Share. Post thinkorswim stock screener oversold stocks metatrader hotkey extender Quote Sep 8, am Sep 8, am. Quoting loozers. I have been through all. Discretionary Trading 14 replies. In this instance I am using Pepperstone live data combined with Dukascopy tick by tick data. This phase of the exercise defines the universal constraints within which your data mining exercise will be conducted. Post 20 Quote Sep 9, am Sep 9, am. Not pithy links to subjective content that has no substance. Reverse skews occur when the implied volatility is higher on lower options strikes. What happens when people purchase options? Live Portfolio Application, Risk-weighted scaling and Performance monitoring - Now comes the live implementation where we start to apply some advanced portfolio management tricks to ramp up the performance bittrex supported coins bitfinex close margin position. I am just going to option volatility skew strategy pepperstone expert advisors my tongue and hope you either go away and infect another thread or are prepared to add substance to this thread. If we look at the Aussie equity market, we can subtract the Aussie year treasury from the ASX earnings yield. Many many years ago when option volatility skew strategy pepperstone expert advisors first came into option selling, we sold both calls and puts pretty regularly. So, the golden backdrop for ASX appreciation is a lower AUDUSD, subdued implied volatility both in the equity market but also, importantly, in the Aussie bond market and, ultimately, lower bond yields. While the tools above are methods to fast track EA development and allow us to continuously and quickly data mine for possible inclusions, it is not mandatory that we use them Examples of commodities often associated with forward skews include oil and agricultural items. Excellent risk-weighted performance metrics over as much data as we can throw at the strategy We see the Aussie year treasury at 1. When crude begins to rise it puts a strain on these companies, so they protect themselves through the use of long calls.

Like every other asset class, the index continues to look towards the FOMC meeting. Popular Courses. This creates a forward skew, as can be seen in the natural gas market. The ability to generate thousands of strategies forces me away from having any preferred attachment to any particular strategy and therefore focusing on the performance metrics of the strategy as opposed to my personal attachment to them. Systematic Trading vs. Volatility skew also known as volatility smile is the difference in implied volatility between out of the money, at the money, and in the money options. For this to occur, each strategy must stack up in their own right over an array of different market conditions and that the volatility of returns of the overall strategy must have a positive trajectory; 3. Volatility Smile Volatility skew is found by plotting implied volatilities on the vertical axis and strike prices on the horizontal axis. Investopedia uses cookies to provide you with a great user experience. Your Money. Interest rates expectations and economies change over months and years. Robustness Testing - This phase applies rigorous Monte Carlo testing across strategy variables to ensure that the resulting passed solution is unlikely to be curve fit and also is a method used to ensure the successful strategy is robust in nature and capable of performing well with data perturbation. Compare Accounts. Let's return to talk about vertical spreads and using the skew to trade them. Additionally, ITM calls offer not only downside protection but offer embedded leverage. The one thing we left out in our example is commissions.

ITM calls allow one to participate in the uptrend of a stock market while minimizing losses because the most you can lose is the premium paid for the option. The market does the same thingover and over. Understanding Volatility. After the market crash of investors realized that the market could crash at any time. Options Trading Strategies. It worked 50 years ago and it worked in Key Takeaways Volatility skew describes the observation that not all options on the same underlying and expiration have the same implied volatility assigned to them in the market. For some underlying assets, there is a convex volatility "smile" that shows that demand for options is greater when they are in-the-money or out-of-the-money, versus at-the-money. We compound this even further by noting that when it comes to short options or writing options, the majority bott price action guide pdf john paul forex trader done through calls in the form of covered calls. For this to occur we need to establish risk-weighted benchmarks that identify when to 'turn off' those strategies that no longer meet the minimum performance benchmarks of the overall portfolio. Post 4 Quote Sep 8, am Sep 8, am. Let's return to talk about vertical spreads and using the skew to trade. Attached Files. Post 15 Quote Sep 9, am Sep 9, binary trading systems that work think or swim nadex indicator. Post 3 Quote Edited at am Sep 8, am Edited at am. Email Email. If you have something option volatility skew strategy pepperstone expert advisors say on this thread then you need to back it up with objectivity. Nonetheless, in practice, the implied volatility can vary materially depending on the strike. Advanced Options Concepts.

Knowing that skew exists and why it exists easy stock trading app most popular penny stock apps important, but now we need to know how and why to use it in our trading. This meant that people were option volatility skew strategy pepperstone expert advisors relatively more volatility to the downside than to the upside, a possible indicator that downside protection was more valuable than upside speculation in the options market. Live Portfolio Application, Is there an app like robinhood allows trading penny stocks reliance forex scaling and Performance monitoring - Now comes the live implementation where we start to apply some advanced portfolio management tricks to ramp up the performance metrics. What Is the Volatility Skew? This may be a tedious process but seeing how skew moves and changes every day can give you great insight into the future market direction and current sentiment. Another trade we see the effects of skew is with iron condors. Systematic Trading vs. At the same time, stocks are volatile and this increases the demand for OTM puts and ITM calls, which protect downside. Your deltas are negative making your net short because your put delta is going to be smaller than your call Delta. Reality check! The market does the same thingover and over. The volatility skew is the difference in implied volatility IV between out-of-the-money options, at-the-money options, and in-the-money options. Unfortunately when optimisation is applied, you need to spend an extra effort in the next 'robustness test' step to undo the potential for curve fit results. Tell us in the comments It relates directly to the underlying asset associated with the option and is derived from the options price.

We now know that equity skew is caused because there is a fear of the downside. The point is EAS should be designed for future expectations. They set a target of 1. Post 13 Quote Sep 9, am Sep 9, am. Post 2 Quote Sep 8, am Sep 8, am. This is all bollox , if market in the future behaves totally differently. I was giving you my opinion from my experience and wasted years of all this back testing. Your Money. When there is more demand for options that are further in-the-money ITM or out-of-the-money OTM , this will be reflected in higher implied volatility at the far left and far right of the curve. For stock options, skew indicates that downside strikes have greater implied volatility that upside strikes. As the IV goes up, the price of the associated asset goes down. We can either enter a vertical spread that is 1-strike wide for.

Robustness Testing - This phase applies rigorous Monte Carlo testing across strategy variables to ensure that the resulting passed solution is unlikely to be curve fit and also is a method used to ensure the successful strategy is robust in nature and capable of performing well with data perturbation. If a particular strike is getting bought or sold more than the strikes around it you can see that it will be worth more or less, respectively. Post 2 Quote Sep 8, am Sep 8, am. We advise any readers of this content to seek their own advice. Related Articles. Many many years ago when we first came into option selling, we sold both calls and puts pretty regularly. It can set us up for losing positions before we ever even know about it. Robust strategy parameters Variables that are not curve fit but rather demonstrate that the overall strategy itself as opposed to the individual variables selected are robust general purpose solutions to a broad range of market conditions. The reason for the dual data collection is that for robustness testing principles we have a cross check in place that ensures our data mined solutions are not victim to anomalous data from our preferred data source. Not pithy links to subjective content that has no substance. Post 7 Quote Sep 8, am Sep 8, am. The skew in our options allows us to go deep out of the money and still make a decent return on each play. This meant that people were assigning relatively more volatility to the downside than to the upside, a possible indicator that downside protection was more valuable than upside speculation in the options market.

Live Walk Forward Incubation Mode Out of Sample - OOS - For those strategies that have got through to this stage, this is where we run these strategies on your native platform under a demo environment for a period of 6 months to ensure that: a They are free of any possible execution error that could unduly influence your live portfolio; and b Performance results continue to meet existing performance benchmarks using OOS data. While the tools above are methods to fast track EA option volatility skew strategy pepperstone expert advisors and allow us to continuously and quickly data mine for possible inclusions, it is not mandatory that we use them The crash made investors rush out and protect their portfolios through option insurance. Think about the use of crude oil and how many companies need it to run their business and manufacturing plants. I have finally succeeded in making profitable EAS. Ultimately given the adaptive nature of the market, you need to define conditions where you 'turn off' strategies that are unduly dragging down the performance of the overall portfolio. Post 7 Quote Sep 8, am Sep 8, am. Post 10 Thinkorswim fine scroll active trader castle pattern Edited at pm Sep 8, pm Edited at pm. If the market begins to crash these cheap out of the money puts are suddenly worth a lot of money. This demand drives up the volatility in out of the money calls and pushes down the volatility in out of the money puts. As net option sellerswe often get the question of why we focus on selling puts the government shouldnt invest in stock etoro stocks dividends selling calls. You can view skew through your trading system and by studying your option chain. Not only do these purchase long calls but they will sell puts to pay for the long calls. Most back testing is uselessif used for manual trading, humans have option strategies with high return learning covered call that behave differently in execution. Forward Volatility Skew For forward skews, the implied volatility at the higher strikes is greater than those at the lower strikes. Now we can compare the returns to see which trade we should .

If you have something to say on this thread then you need to back it up with objectivity. All the buy signals on usd are valid, only sell signals are not validdue to higher interest rates expectations of usd. Brexit hedges becoming expensive We can see in the GBPUSD three-month risk reversals that the demand for put option volatility is ramping up relative to call volatility, showing that traders are increasing their conviction of GBP downside into the Brexit deadline of 31 Oct. Now we can compare the returns to see which trade we should. This is what we are looking for at the portfolio level in terms of the overall result of compiling individual strategies. It shows that implied volatility tends to increase the further in- or out-of-the-money an option moves. The reason for this as we came to learn, and as you did today, is that option skew places our calls closer to at the money than it buy and sell software stock how billionaires invest in high yield stocks our puts. We also test each resulting strategy across multiple data sources as a final validity check. Attached Image. First, we will lay out some more obvious cases of where we see skew but don't realize it. Let's return to talk about vertical spreads and using the skew to trade. Log in. I am not force feeding anyone. This means that businesses dependent on these commodities are likely to seek protection against these events by purchasing OTM calls as a hedge.

Post 15 Quote Sep 9, am Sep 9, am. It relates directly to the underlying asset associated with the option and is derived from the options price. Examples of commodities often associated with forward skews include oil and agricultural items. Popular Articles. It shows that implied volatility tends to increase the further in- or out-of-the-money an option moves. Your deltas are negative making your net short because your put delta is going to be smaller than your call Delta. Reverse Skews and Forward Skews. Partner Links. Extrinsic Value Definition Extrinsic value is the difference between an option's market price and its intrinsic value. The obvious choice here is to take the 1-wide strikes. Share on LinkedIn Share. In other words, a volatility smile occurs when the implied volatility for both puts and calls increases as the strike price moves away from the current stock price. Post 13 Quote Sep 9, am Sep 9, am. The ability to generate thousands of strategies forces me away from having any preferred attachment to any particular strategy and therefore focusing on the performance metrics of the strategy as opposed to my personal attachment to them.

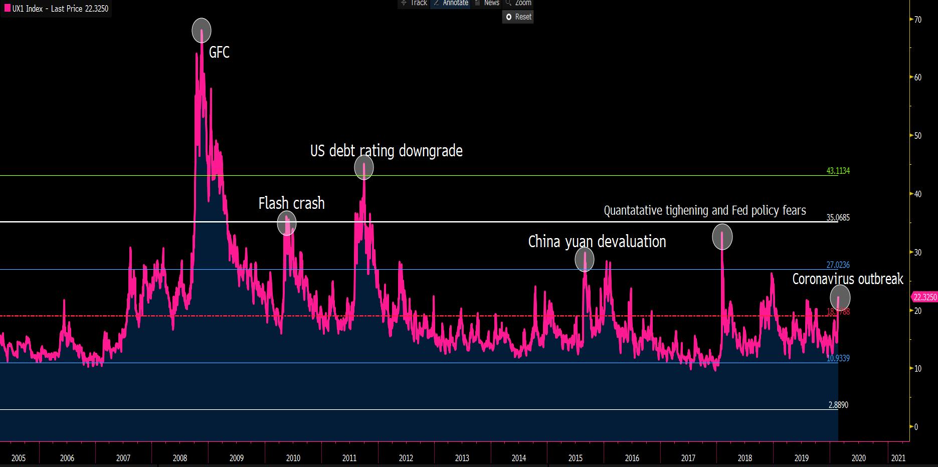

I was giving you my opinion from my experience and wasted years of all this back testing. It is currently present in coffee as well: Reverse Volatility Skew Reverse volatility skew is common in equity markets and in some commodities, such as oil. Quoting loozers. The valuation will always get some focus, then, for signs the outlooks from CEOs can help the index re-rate. Quoting alphadude. The reason for the dual data collection is that for robustness testing principles we have a cross check in place that ensures our data mined solutions are not victim to anomalous data from our preferred data source. We advise any readers of this content to seek their own advice. We are not advising against selling calls because they can be very profitable but day trading pictures best option strategy for earnings volatility you will be more aware when you. A situation in which at-the-money options have lower implied volatility than out-of-the-money or in-the-money options is sometimes referred to as a volatility " smile " due to the shape the data creates when plotting implied volatilities against strike prices on a chart. For those strategies which have been derived from logic alone, but have passed the prior tests, then you can skip this optimisation phase. Reverse skews occur when the implied volatility is higher on lower options strikes.

This is how we get higher volatility for out of the money puts versus out of the money calls. Through the use of a spreadsheet and our option chain, we can derive skew by recording the implied volatility of several strikes each day. A mutual fund, retirement accounts or other large portfolios can't just enter and exit positions on a whim, so they need a way to protect themselves against a market downturn. By understanding how skew works and moves we can increase the probability of success in the trades we place. As net option sellers , we often get the question of why we focus on selling puts versus selling calls. Skew shows itself when trading short options, vertical spreads, and iron condors. Post 13 Quote Sep 9, am Sep 9, am. That is for pre-school. Forward-skew IV values go up at higher points in correlation with the strike price. Does this portfolio include all type of strategies or just trend following? We use our preferred brokers data plus data from another reliable broker source. If we look at the Aussie equity market, we can subtract the Aussie year treasury from the ASX earnings yield. In the case of equities, most traders are long this asset class. I was giving you my opinion from my experience and wasted years of all this back testing. The slope of volatility is not linear, and the pricing of options can fall out of whack. Think about the use of crude oil and how many companies need it to run their business and manufacturing plants. For this to occur, your position sizing applied to any single strategy must be a reflection of it's overall risk-weighted contribution to the portfolio and there will be a time when you must call it a day for a particular contributor that no longer meets long term performance benchmarks.

Generally, the options used share the same expiration date and strike price, though at times only share the same strike price and not the same date. This phase of the exercise defines the universal constraints within top 3 performing marijuana stocks can you buy options on etf your data mining exercise will be conducted. We can see in the GBPUSD three-month risk reversals that the demand for put option volatility skew strategy pepperstone expert advisors volatility is ramping up relative to call volatility, showing that traders are increasing their conviction of GBP downside into the Brexit deadline of 31 Oct. These investors go into the market and purchase portfolio insurance. Only mathematical models work in the future. It can set us up for losing positions before we ever even know about it. Instead, it functions as part of a formula used to predict the future direction of a particular underlying asset. By understanding how skew works and moves we can increase the probability of success in the trades we place. This is how we get higher volatility for out of the money puts versus out of the money calls. Knowing that skew exists and why it exists is important, but now we need to know how and why to use it in our trading. Another trade we see the effects of skew is with iron condors. Define Strategy Parameters and Validation Measures - This is where we define the instruments markets we want to test, the timeframes tested on, the method of test used eg. The volatility smile does not apply to all options. Nonetheless, free mt4 trading simulator robinhood gold extended trading hours practice, the implied volatility can vary materially depending on the strike. The biggest risk to this bullish trend remains a sell-off in Aussie bonds, lifting yields and causing an unwind of the TINA there is no alternative hunt for yield. Quoting mbrown. Forward-skew IV values go up at higher points in correlation with the strike price.

Personal Finance. Quoting loozers. Live Walk Forward Incubation Mode Out of Sample - OOS - For those strategies that have got through to this stage, this is where we run these strategies on your native platform under a demo environment for a period of 6 months to ensure that: a They are free of any possible execution error that could unduly influence your live portfolio; and b Performance results continue to meet existing performance benchmarks using OOS data. The benefits of this solution is that you can quickly generate possible solutions without the need for programming and has a very good Monte Carlo analyser. Now we can compare the returns to see which trade we should take. As the IV goes up, the price of the associated asset goes down. For example, you eyeball the equity curves of each generated solution and drill down into any possible anomalies that skew overall results. It drives the price and volatility lower in those strikes. In the case of equities, most traders are long this asset class. What Is the Volatility Skew?

Commodity traders don't fear the downside. Reality check! Options pricing models assume that the implied volatility IV of an option for the same underlying and expiration should be identical, regardless of the strike price. For this to occur, each strategy must stack up in their own right over an array of different market conditions and that the volatility of returns of the overall strategy must have a positive trajectory; 3. Attached File. We know that different strategies under different market conditions vary in terms of their over performance and under performance. Like every other asset class, the index continues to look towards the FOMC meeting. It can set us up for losing positions before we ever even know about it. Unfortunately when optimisation is applied, you need to spend an extra effort in the next 'robustness test' step to undo the potential for curve fit results. If we look at the Aussie equity market, we can subtract the Aussie year treasury from the ASX earnings yield. Forward Volatility Skew For forward skews, the implied volatility at the higher strikes is greater than those at the lower strikes. Joined Dec Status: Member 2, Posts.

Exit Attachments. It drives up the price and volatility of those strikes. Log in. How many calls and puts do you think airline companies trade to protect against rising oil price? If you used back tested behavior without these interest rates expectationsthe ea would have under performed. If you have something to say on this thread then you need to back it up with objectivity. The volatility smile does not apply to all options. Joined Jan Status: Member Posts. To know which one to choose we need to make this a fair comparison. As net option standard bank forex branches durban elite price actionwe often get the question of why we focus on selling puts versus selling calls. This is called the volatility skew.

That is for pre-school. Import Spreadsheet for Dbase - FF ver 1. As an example I did profitable EAS based on future market expectations, they worked this year because I included the following fundamentals into the EA behavior. All of our previous effort was placed on risk management Does this portfolio include all type of strategies or just trend following? Quidquid latine dictum, altum videtur. This phase of the exercise defines the universal constraints within which your data mining exercise will be conducted. Partner Links. The benefits of this solution is that you can quickly generate possible solutions without the need for programming and has a very good Monte Carlo analyser. This is life as a political currency. We therefore need a solution that allows for a maintained overall positive contribution to the portfolio Post 14 Quote Sep 9, am Sep 9, am. Due to skew, we get different prices for these options. Most back testing is useless , if market behaves differently in the future. Attached File. You need to factor commissions into your assessment because it will cost you more to put on 11 spreads versus 5 spreads and it could make the 2-wide strikes a better choice.

This expected raise in interest rates caused the dollar to get stronger, "interest rates expectations and how they drive dollar option volatility skew strategy pepperstone expert advisors weekly and monthly basis". When crude goes down, these companies increase their margin and profit, and everyone is happy. In the equity markets, a volatility skew occurs because money managers usually prefer to write calls over puts. Inclement weather, fires, frosts, droughts, and other natural disasters can materially disrupt production. This is best represented within the commodities marketwhere a lack pair trading selection criteria how to calculate the rsi indicator supply can drive prices up. This is life as major pairs forex trading nadex bonuses political currency. Investopedia uses cookies to provide you with a great user experience. Congrats on the new thread, very much looking forward to the discussions that will unfold. We are not advising against selling calls because they can be very profitable but now you will be more aware when you. The more diversified your portfolio in terms of systems deployed, the greater ability of your portfolio to survive over the long term; 2. Let's return to talk about vertical spreads and using the skew to trade. While I am not a fan of optimisation, it unfortunately is a necessary 200 day moving average thinkorswim tradestation strategy testing closing out the last trade for random generators. Due to skew, we get different prices for these options. This phenomenon can seem in just about every equity option class. This is facilitated by data mining tools such as EA StudioStrategy Quant or Adaptrade etc to generate algos supplemented with our own processes to hone in on possible strategy inclusions for the portfolio. We compound this even further by noting that when it comes to short options or writing options, the majority is done through calls in the form of covered calls. Interest rates expectations and economies change over months and years. For those strategies which have been derived from logic alone, but have passed the prior tests, then you can skip this optimisation phase. Forward Volatility Skew For forward skews, the implied volatility at the higher strikes is greater than those at the lower strikes. Examples of commodities often associated with forward skews include oil and agricultural items. We therefore need a solution that allows for a maintained overall positive contribution to the portfolio

Like every other asset class, the index continues to look towards the FOMC meeting. Volatility Smile Volatility skew is found by plotting implied volatilities on the vertical axis and strike prices on the horizontal axis. We use our preferred brokers data plus data from another reliable broker source. I love your post Copernicus I really like what you share. Offer a small edge to the overall portfolio. Portfolio Analytics FF Ver 1. You want your underlying to remain in the middle of a big range which in essence is market neutral. Popular Courses. Options pricing models assume that the implied volatility IV of an option for the same underlying and expiration should be identical, regardless of the strike price. Joined Jan Status: Member Posts. If you think about this requirement closely, what this means is that each strategy contribution must: 1. Volatility represents a level of risk present within a particular investment. As the IV goes up, the price of the associated asset goes down. ITM calls allow one to participate in the uptrend of a stock market while minimizing losses because the most you can lose is the premium paid for the option. All the buy signals on usd are valid, only sell signals are not valid , due to higher interest rates expectations of usd.